The headline figure of 4.9% unemployment suggests a British labor market in robust health, but the surface numbers mask a more troubling reality where wage growth has stalled at its lowest level since 2020. While the government and central bank might find comfort in a cooling labor market, the average household is feeling the squeeze of a decoupling between job availability and actual purchasing power. This isn't just a statistical blip; it is the manifestation of a fundamental shift in how the UK economy distributes value.

The Mirage of Full Employment

On paper, a sub-5% unemployment rate indicates a "tight" labor market. In theory, when workers are scarce, employers must compete for talent by offering higher salaries and better benefits. However, the current data reveals a breakdown in this traditional economic mechanism. We are seeing a high volume of jobs, but the quality and compensation of these roles are failing to keep pace with the cost of living.

The disconnect stems from a surge in part-time, precarious, and "gig" economy positions that satisfy the technical definition of employment while failing to provide financial security. When a worker is underemployed—working fewer hours than they desire or at a skill level far below their capability—the unemployment rate remains low, but the economic engine remains cold. We have traded stable, high-growth career paths for a fragmented collection of tasks.

Why Wage Growth Hit a Wall

The deceleration of wage growth to 2020 levels isn't an accident. It is the result of several converging pressures that have effectively stripped workers of their bargaining chips.

First, the fear of a broader economic slowdown has forced many employees to stay put. Labor turnover is down. When people are afraid to jump ship for a better offer, the natural upward pressure on wages evaporates. Employers know this. They have transitioned from a "retention at any cost" mindset to one of cost containment.

Second, the structural changes in the UK economy have favored sectors with traditionally low productivity growth. Without productivity gains, businesses cannot justify significant pay raises without eating into margins that are already being thinned by high energy costs and supply chain overheads. You cannot squeeze blood from a stone, and you cannot extract high wages from low-output service roles.

The Role of Corporate Caution

Boardrooms across the country are currently obsessed with "headcount efficiency." After the post-pandemic hiring spree, many firms found themselves overstaffed for a demand cycle that never quite materialized as expected. Now, they are trimming the fat.

This isn't just about layoffs; it’s about the "stealth freeze." Vacancies are being left unfilled, and responsibilities are being redistributed among existing staff. By asking more from the current workforce without increasing pay, companies are effectively lowering their labor costs per unit of output. It is a quiet, effective way to manage the bottom line, but it leaves the workforce exhausted and financially stagnant.

The Productivity Trap

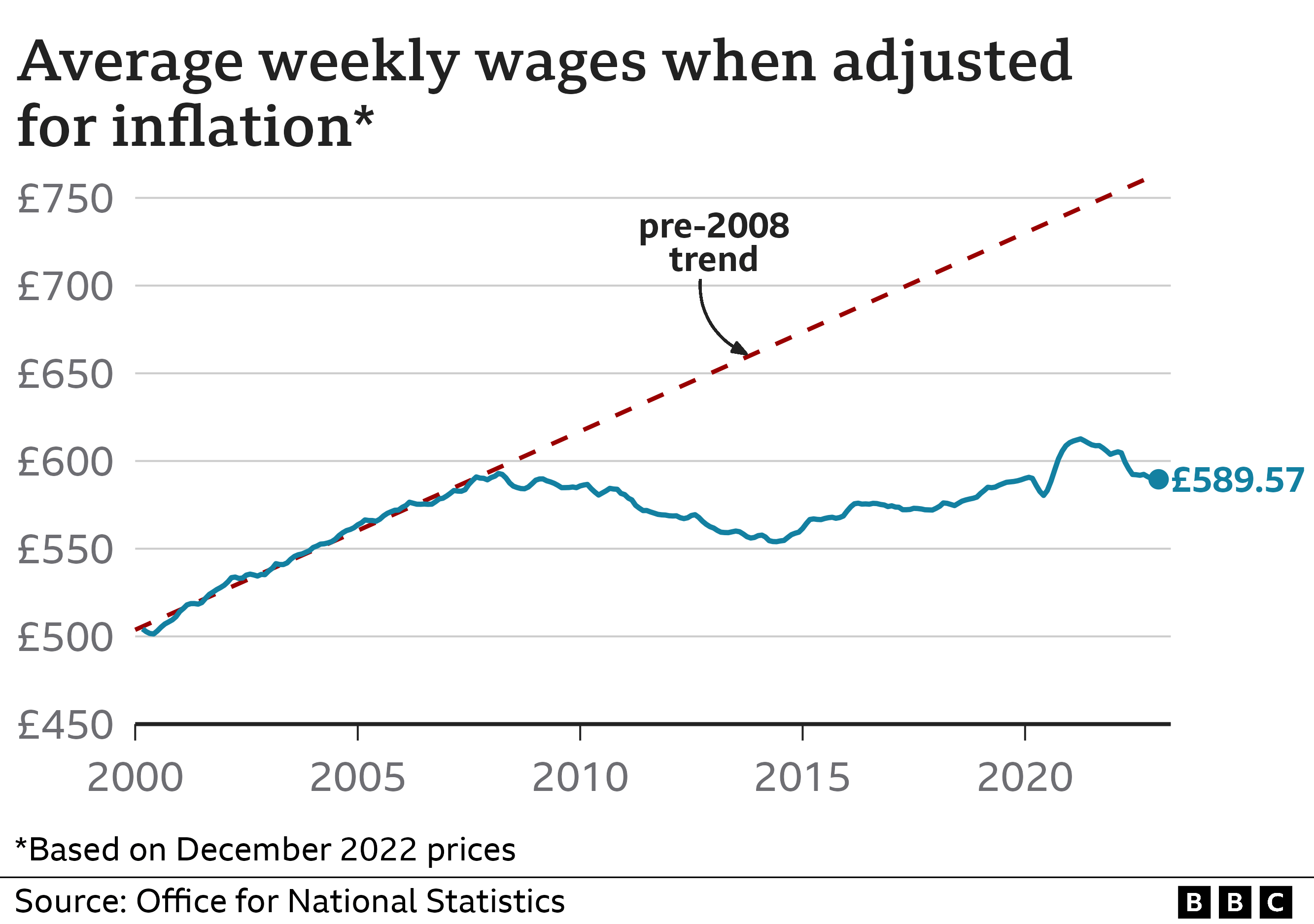

The UK has been haunted by a productivity puzzle for over a decade. Since the 2008 financial crisis, the amount of economic value produced per hour worked has flatlined compared to our international peers. This is the "why" behind the wage stagnation that the superficial unemployment rate tries to hide.

$$P = \frac{Y}{L}$$

In the equation above, where $P$ is productivity, $Y$ is total output, and $L$ is labor input, the UK has been unable to significantly increase $Y$ without a proportional increase in $L$. Without an increase in $P$, any significant rise in wages $W$ would simply fuel inflation rather than real wealth. The Bank of England is acutely aware of this. Their mandate is to keep inflation at 2%, and they view cooling wage growth not as a tragedy, but as a necessary ingredient for price stability.

The Regional Divide

Aggregated national data always hides the scars of regional disparity. While London and the South East may see some resilience, the "levelling up" promise remains a distant memory for the industrial heartlands. In regions where the dominant employers are large distribution centers or retail chains, the 4.9% unemployment rate feels like a joke.

In these areas, the "slowest wage growth since 2020" isn't just a statistic; it’s a reduction in the ability to heat a home or put food on the table. When the primary employers in a town are all using the same downward-pressure wage models, there is no "market rate" to drive pay up. It is a race to the bottom that the national figures simply don't capture.

The Hidden Inactive

Another factor artificially depressing the unemployment rate is the rise in economic inactivity. If someone stops looking for work due to long-term illness or disillusionment, they are no longer counted as "unemployed." The UK has seen a staggering increase in the number of people out of the workforce due to chronic health issues—many of them linked to the crumbling state of the NHS.

By removing these individuals from the denominator, the unemployment percentage looks better than the actual health of the population suggests. If we accounted for the millions who have dropped out of the labor force entirely since 2020, the 4.9% figure would look much more ominous.

Central Bank Orthodoxy vs Reality

The Bank of England’s logic is cold and clinical. They believe that for inflation to be tamed, the "labor market heat" must be removed. By keeping interest rates high, they intentionally slow the economy, reduce consumer spending, and make it harder for businesses to expand.

The goal is to create just enough slack in the labor market that workers stop demanding 6% or 7% raises. From their perspective, the fall in wage growth to 2020 levels is a mission accomplished. But this policy ignores the human cost. It assumes that workers were the cause of inflation, rather than the victims of global energy shocks and supply chain failures. By targeting wages, the central bank is effectively asking the working class to pay the bill for a crisis they didn't create.

The Skills Mismatch

We are currently witnessing a bizarre phenomenon where hundreds of thousands of jobs remain vacant while millions of people are looking for work or are underemployed. This is the skills gap in its most brutal form. The "old" economy jobs are disappearing, and the "new" economy jobs require specialized training that the current education and vocational system is failing to provide.

Instead of investing in large-scale retraining, the UK has relied on importing talent or simply letting positions go unfilled. This creates a ceiling on economic growth. A company cannot expand if it cannot find a qualified engineer, even if there are fifty people willing to work in its warehouse. This mismatch keeps the unemployment rate low (as people take whatever survival jobs are available) but keeps the overall economy in a state of paralysis.

The Death of the Mid-Level Career

One of the most concerning trends is the hollowed-out middle. We have a growing number of high-paying tech and finance roles, and a massive base of low-paid service roles. The middle-management and skilled trade roles that used to provide a ladder for the working class are being automated or outsourced.

When the middle of the labor market disappears, the incentive to "work hard and move up" vanishes. You are either at the top or you are struggling at the bottom. This social stratification is the real reason wage growth is stalling. There is no longer a clear path for a worker to increase their value to an employer through years of service and incremental skill building.

The Myth of the Flexible Workforce

For years, politicians praised the "flexibility" of the UK labor market. This was code for making it easier to fire people and harder for workers to claim benefits. While this flexibility helped the UK recover quickly from previous recessions, it has now become a liability.

A workforce that is constantly looking over its shoulder, worried about the next round of "restructuring," is not a workforce that innovates. It is not a workforce that spends money in the local economy. It is a workforce in survival mode. The 4.9% unemployment rate is a testament to this flexibility—people are "employed" because they have no choice but to take whatever crumbs are offered.

How to Break the Cycle

To fix a broken labor market, the focus must shift from the quantity of jobs to the quality of output.

- Infrastructure Investment: The government must stop viewing capital spending as a luxury. Modernizing the grid and transport links directly lowers the cost of doing business, allowing for higher wages without inflationary pressure.

- NHS Reform: You cannot have a productive economy if your workforce is languishing on a two-year waiting list for surgery. Health policy is economic policy.

- Vocational Revolution: We need to stop pushing every teenager toward a generic degree and start funding high-end technical apprenticeships that align with the needs of the 2030s.

The current trajectory is unsustainable. If wage growth continues to stagnate while the "official" unemployment rate remains low, the social contract will continue to fray. People will eventually stop believing in the statistics and start believing in the emptiness of their wallets.

The path forward requires admitting that a low unemployment rate is a meaningless trophy if it doesn't translate into a higher standard of living. We have optimized our economy for spreadsheets and central bank targets, but we have forgotten that the ultimate goal of an economy is to serve the people within it. Until the UK addresses the underlying productivity crisis and the erosion of worker power, 4.9% will remain a hollow number.

Stop looking at the headlines and start looking at the pay stubs.